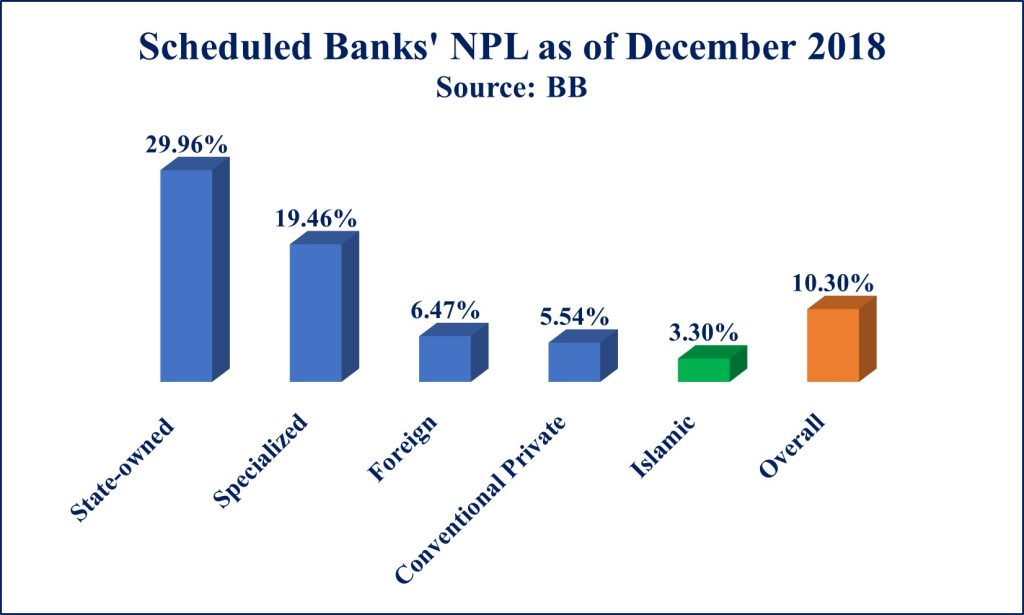

At present, non-performing loan (NPL) is the most talked about issue in the banking sector of Bangladesh. The amount of default loans hit nearly BDT 1 lakh crore (11.45% of disbursed loans) at the end of September 2018 for the first time in the country’s history. From 2009 to 2018, the amount of NPL has been increased by more than 300%. Currently, we have 61 scheduled banks in Bangladesh. Overall banking sector’s NPL stood at 10.30% of total loans as of December 2018. It was 29.96% for state-owned commercial banks, 19.46% for specialized banks, 6.47% for foreign commercial banks, 5.54% for conventional private commercial banks, and 3.3% for Islamic banks (source: Bangladesh Bank).

The percentages indicate that Islamic banks are more efficient in monitoring their loans compared to other banks. In theory, NPL is inversely correlated to bank profitability. Many studies on the conventional banking industry of Bangladesh found the negative relationship between NPL and profitability. However, one of my studies on country’s Islamic banking industry observed that bad loans do not adversely affect the profitability (you may read the study here). I concluded that the average NPL of Islamic banking industry is very low (3.3%) compared to NPL of overall banking industry of Bangladesh (10.30%). Therefore, such tight control of loan losses could not affect the profitability severely. But how do the Islamic banks control loan losses?

Theoretically, Islamic banks do not disburse loans to clients. They run their activities according to Islami Shariah-based principles, i.e. profit-loss sharing (PLS) mode. Islamic banks earn money through investment in businesses and individuals. The funds for the investment come from the banks’ equity and customers’ deposits. The depositors are entitled to a share of the bank’s profit or loss based on a certain predetermined percentage.

An Islamic bank may purchase goods and services on behalf of the clients and resell those things to them for a profit. Therefore, the clients will not be able to spend the fund into unproductive sectors, hence the probability of default is minimized. On the other hand, when they invest in a business, they should be very cautious about quality of the investment. Since Islamic banks operate on a PLS basis, deterioration of investment income will lead to a lower profit rate to the depositors which might force the depositors to switch to other banks. In addition to that, in conventional banking, when interest rate raises, it increases the cost of fund. However, a business cannot always adjust the price of the goods and services according to the interest cost which ultimately causes a huge loss to the business and thus the chance of default is increased. Islamic banks are protected from such risks. Moreover, Islamic banks invest in real economy. They usually avoid investing in securities or other financial instruments. Therefore, speculative risk is less in this sector and they are more resilient to financial crisis.

To conclude, both Islamic and conventional banks operate under the same legal and regulatory framework of Bangladesh Bank. Typically, Islamic banks imitate the ways in which conventional banks operate. However, the tools of the Islamic banking system have the ability to control the bad debts. Therefore, it is suggested that conventional banks should reproduce these tools by making necessary changes in accordance with the nature of their operations to minimize the probability of loan default.